Your top questions answered!

In our 3rd Quarter 2023 market commentary, Hillary Sunderland, CFA®, CKA®, Chief Investment Officer of Beacon Wealth Consultants and LightPoint Portfolios, gives a market and economic update and answers some common questions and we’ve heard from clients including:

- Given attractive yields on certificates of deposit, why shouldn’t I just sell out of my investments and invest in CDs instead?

- Is inflation actually receding because it sure doesn’t feel like it?

- The market has been moving sideways for two years. How long do I need to stay invested to reap the benefits of a diversified portfolio?

- What is your outlook for the rest of the year?

Watch the video for answers to these questions and our thoughts on the market!

Full transcript below.

Transcript

Hi, my name is Hillary Sunderland and I’m the Chief Investment Officer of Beacon Wealth Consultants and LightPoint Portfolios. Thank you for being a valued client of ours.

For this quarterly commentary, I’m going to give you a little backdrop on what happened in the market over the last couple of months, and then I’ll jump into answering some of the most commonly asked questions that I’ve received from clients over the last few weeks. So let’s go ahead and get started.

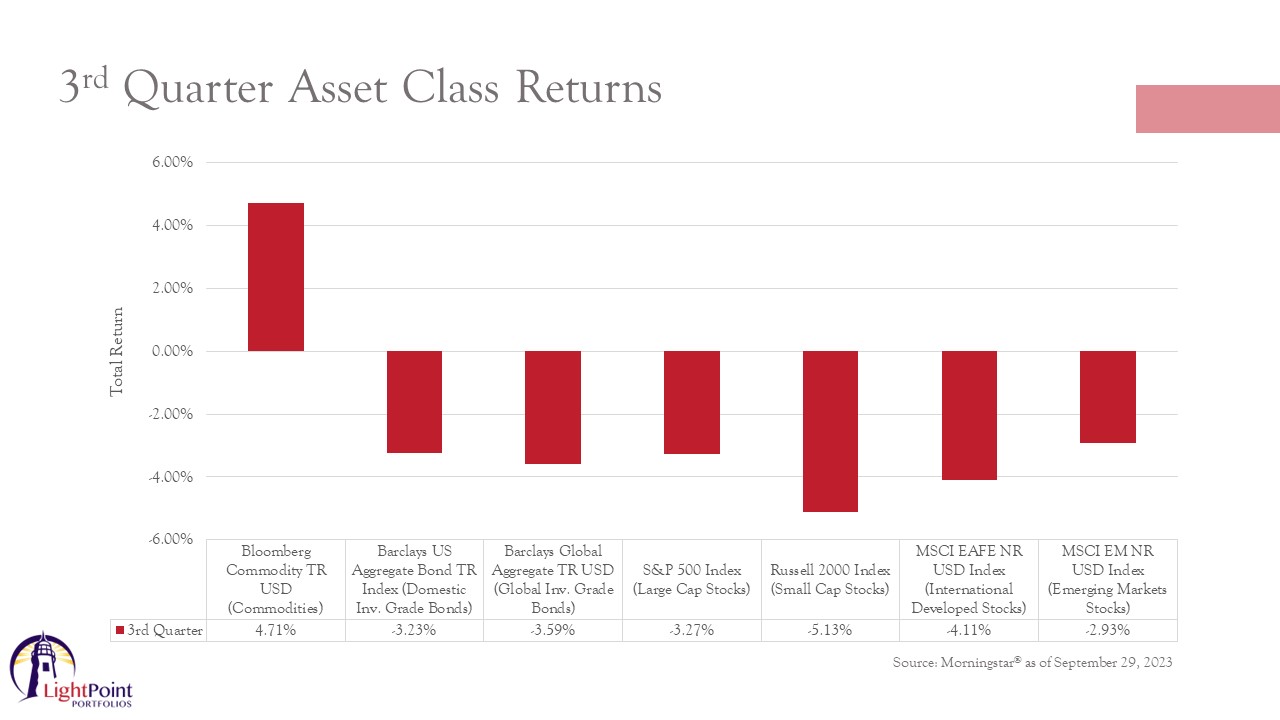

Let’s start by looking at the returns for the third quarter of 2023. I’m going to move from left to right across this slide.

So to start, commodities had the strongest quarter by far of the major asset classes. This gain can be attributed to higher energy prices, which jumped as OPEC supply cuts raise concerns of an imbalance in the oil market. Now, it’s important to note here that the recent rise in oil prices is not due to a surge in demand globally or in the US and the US oil consumption has actually gone down over the last few years and we remain a net exporter of oil.

US oil production has increased by almost 11% since 2019. However, over the same time period, both OPEC and Russia have decreased production by an almost offsetting amount. So this temporary gyration in the oil market doesn’t materially change our outlook for inflation because we do believe that those supply and demand dynamics will come back into balance soon.

Moving on, the US fixed income markets struggled as treasury yields climbed to their highest level since 2007 on the back of strong economic data and messaging from the Federal Reserve that they expect to keep interest rates higher for longer.

It was a similar story for global fixed income as yields moved higher in Europe as well. Given the pullback and bond prices, as interest rates adjusted higher, returns were negative for both domestic and global fixed income indices.

The Federal Reserve’s decision to keep interest rates higher for longer also impacted the equity markets, higher interest rates, increased borrowing costs for companies which can hurt future cash flows and result in lower stock prices, especially in growth stocks.

Additionally, while overall earnings came in stronger than expected, corporate guidance was pessimistic. As a result, the broad large cap and small cap stock indices, the S&P 500 and the Russell 2000 Index shown here, they were both down single digits for the quarter.

On the international side, a stronger US dollar and weakening growth in Europe and China weighed on returns. However, India and Japan were bright spots and emerging markets outpaced developed markets for the quarter.

Now, you may be wondering with both the stock and the bond markets declining, once again, is this an ominous sign of more bad things come. As an investor, it’s important to put the recent declines into context. From a behavioral perspective, we often believe that returns on our portfolios should be moving up in a straight line, but that’s not normal.

On average, we see a pullback in the market of at least 5% about every 14 weeks or a little over three times per year.

We usually see a correction defined as a drop of at least 10% from a recent high once per year. What we’ve had so far since July is a pullback of about 7%, which is normal in the context of investing.

The fact of the matter is that investing often feels lousy and it’s better to take a longer term perspective. Just because both stocks and bonds were down last quarter doesn’t mean that they will continue to fall. This line of reasoning is called recency bias. And recency bias is when we believe that more recent results are indicative of the future and it’s a very backward looking approach to investing.

We’re going to turn now to answering some of the most commonly asked questions I have received from clients over the last few weeks, and I’m going to start with the one that I think has its roots in recency bias because people are afraid that the returns of last quarter will continue.

That question I’ve been receiving is: given attractive yields on certificates of deposit, why shouldn’t I just sell out of my investments and invest in CDs instead?

Well, for starters, it is correct that CDs are yielding more today than they have been for the last 15 years. You can get a yield of just over 5% by purchasing a 12 month cd. This may be a prudent approach for a very short-term need.

However, your investment accounts generally have a much longer time horizon, and there is always the opportunity cost that you need to take into consideration. So there’s really two key questions to ask here. The first is, what are you not investing in to get the exposure to the return of the CD and second, and how is not investing in those assets going to affect your long-term financial plan?

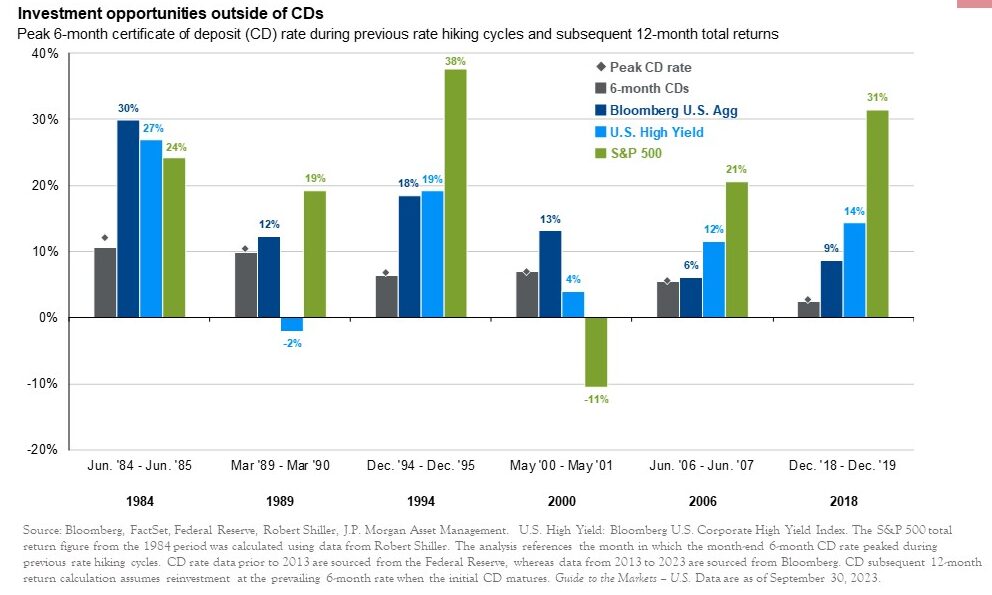

This chart looks at the last six interest rate hiking cycles, and let me take a moment to explain how to read this chart because it is a little busy. For each cycle, the gray diamond is the peak CD rate of that cycle. The gray bar shows the subsequent 12 month total return investors received by buying six month CDs at peak rates.

The dark blue bar represents the subsequent 12 month return of the domestic bond market.

The light blue bar shows the performance of high yield bonds, which we generally have minimal exposure to in our portfolios, so I’m not going to comment on that asset class very much.

And the green bar shows a subsequent 12 month return of the S&P 500 index. What you will notice is that in every single interest rate hiking cycle by staying invested in fixed income, the dark blue bar ,rather than CDs, the gray bar, investors earn higher and sometimes substantially higher returns in comparison to investors in CDs in the subsequent 12 months.

Similarly, an investment in stocks, again, that’s the green bar here outperformed the return of CDs and five out of the six hiking cycles. The exception was the dotcom bust of 2000. Of those five times that stocks outperformed return of CDs, it did so by a very substantial margin. In all cases, the return of stocks was at least double that of CDs and in some cases like 1994 and 2018, well more than double the return of CDs.

While past performance is no guarantee of future results, I believe that the odds are very much in your favor if you stay invested for the next 12 months, despite the enticing yield you’re seeing on CDs today. The reason for this is we have a totally different starting point for fixed income today than we did heading into 2022.

This is not the low yield regime that characterized the last decade of bond investing. Mathematically, the silver lining of all of those rate hikes over the last year was that it gave us a very good yield cushion.

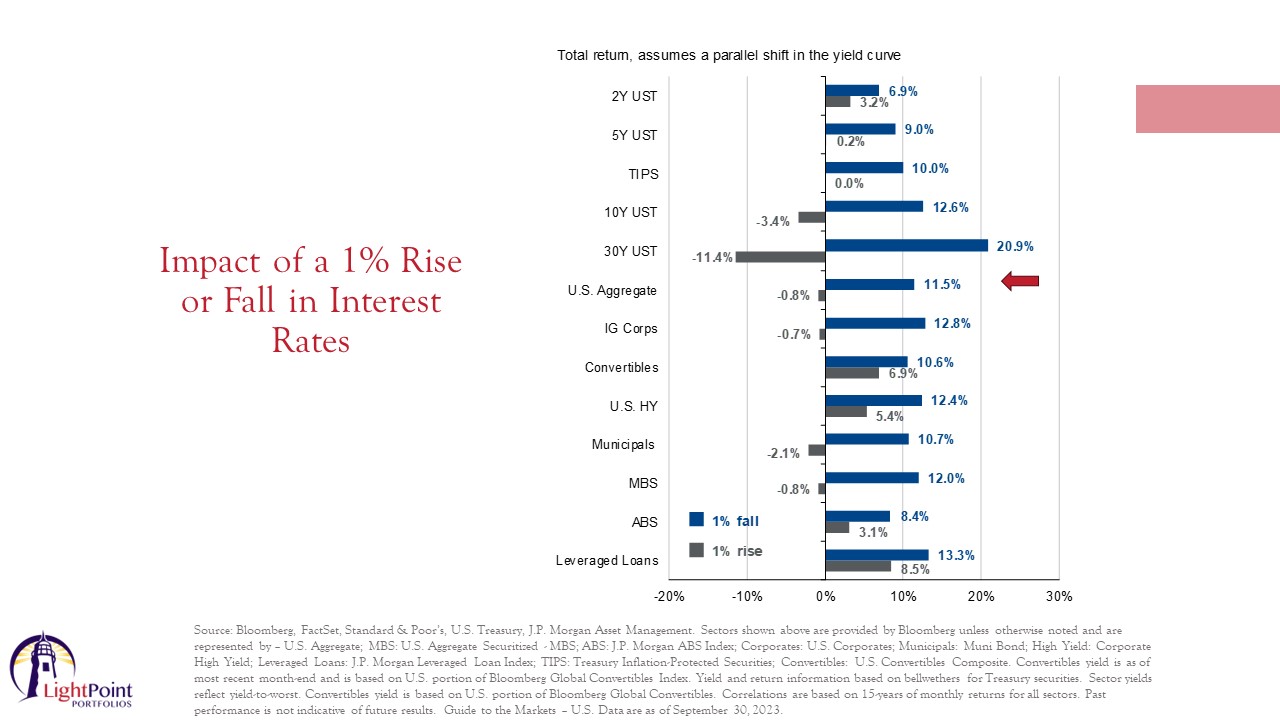

So consider the broad domestic bond market, which is what this red arrow is pointing toward here. Historically, about 90% of your return on a bond investment comes from the interest income, and the broad bond market is currently yielding about 5.39%, which by the way is more than what you can get on a six to 12 month CD.

If nothing happens to interest rates, all else being equal, you will clip this coupon and earn this income over time. Now, assume that a recession hits within the next year. If that occurs, the Federal Reserve will have to cut interest rates in order to stimulate the economy.

If you own a CD at a bank, it will mature and you will have to reinvest it at a lower yield. This is called reinvestment risk. However, when you own fixed income that trades in the secondary market, which is the exposure you get with bond funds or ETFs when you invest with us, if interest rates decline by 1% across the curve, the total return of this index would be 11.5% because as interest rates decline, the price of the bonds you hold goes up.

So there is a capital appreciation component at play. So you may be wondering, well, Hillary, what if you’re wrong? And the Federal Reserve raises interest rates another 1%, won’t that be a repeat of 2022 when bond asset classes declined by double digits?

And the simple answer to that is no. The yield today on the broad bond market index is substantially higher than it was entering 2022. And this gives us what we call a yield cushion, which is essentially a buffer against significant price declines. So in the unlikely scenario, we view as unlikely that anyway that the Fed does raise rates a full 1%. The decline would only be 0.8%, all else being equal. So to summarize, we believe we are already at or near peak interest rates for this cycle. And as such, the road ahead for fixed income is remarkably different than the road behind us.

If you sell out of your portfolio now to buy short-term CDs, you will likely derail your long-term financial plan. Given that short-term CDs will likely not keep pace to the return needed to meet your long-term financial goals. We believe that there is much better total return potential in other asset classes. And so as a prudent investor, you always need to take into consideration what the opportunity cost is of making a financial decision.

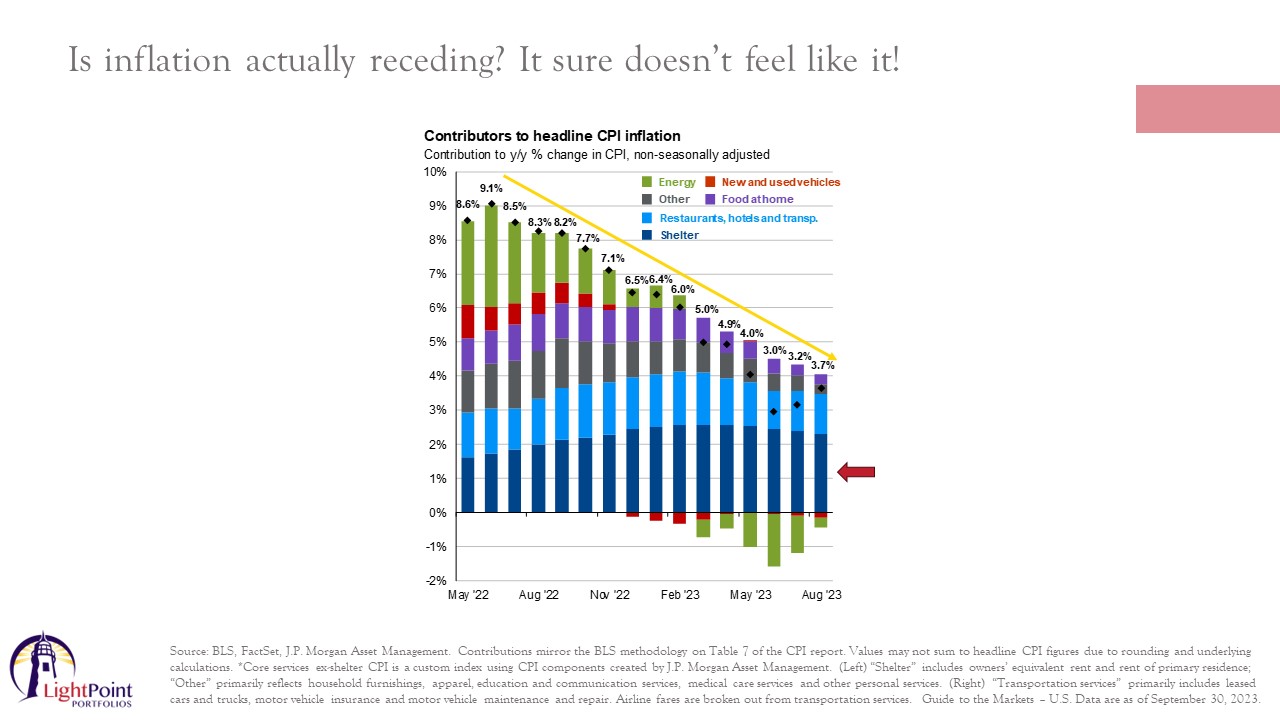

Okay, so let’s move on to the next question I’ve been receiving. Is inflation actually receding because it sure doesn’t feel like it?

Yes, inflation is receding and we are in a substantially better position today than we were in 2022. Annualized inflation has fallen to below 4% from a high of almost 9% last summer. The area that does remain elevated is shelter, the dark blue part of this chart, but that is also finally starting to level off as components such as rent tend to ease with a significant lag.

Included in shelter is a category called transportation services, which includes components such as auto insurance premium, and this area has remained fairly sticky. The cost of auto repairs and parts are more costly than before. Additionally, claims related to natural disasters such as hail damage, hurricanes and wildfires are up quite a bit, which has led to an increase in claims. And when insurance companies have a large increase in claims, they pass on that cost to consumers, which is why you have likely received an increase in your auto insurance premiums, as have I as of late.

So that’s one component that we’re watching closely. But overall, while inflation is still running higher than we would like, it is gradually falling to much more manageable levels and we do expect inflation to decline to 3% year over year by the end of 2023.

So why doesn’t it feel like inflation is falling?

Well, most of this probably has to do with how you think about inflation. So remember, inflation represents the rate of price increases. So when I say that inflation is slowing, that means that prices are increasing at a decreasing rate.

That means that the price of a meal at a restaurant is not going up at the same rate it was before. It does not mean that the price of a meal is going down, that would be deflation. And as good as lower prices sound, it’s actually worse about deflation than inflation. So I guess in a sense, we should count our blessings.

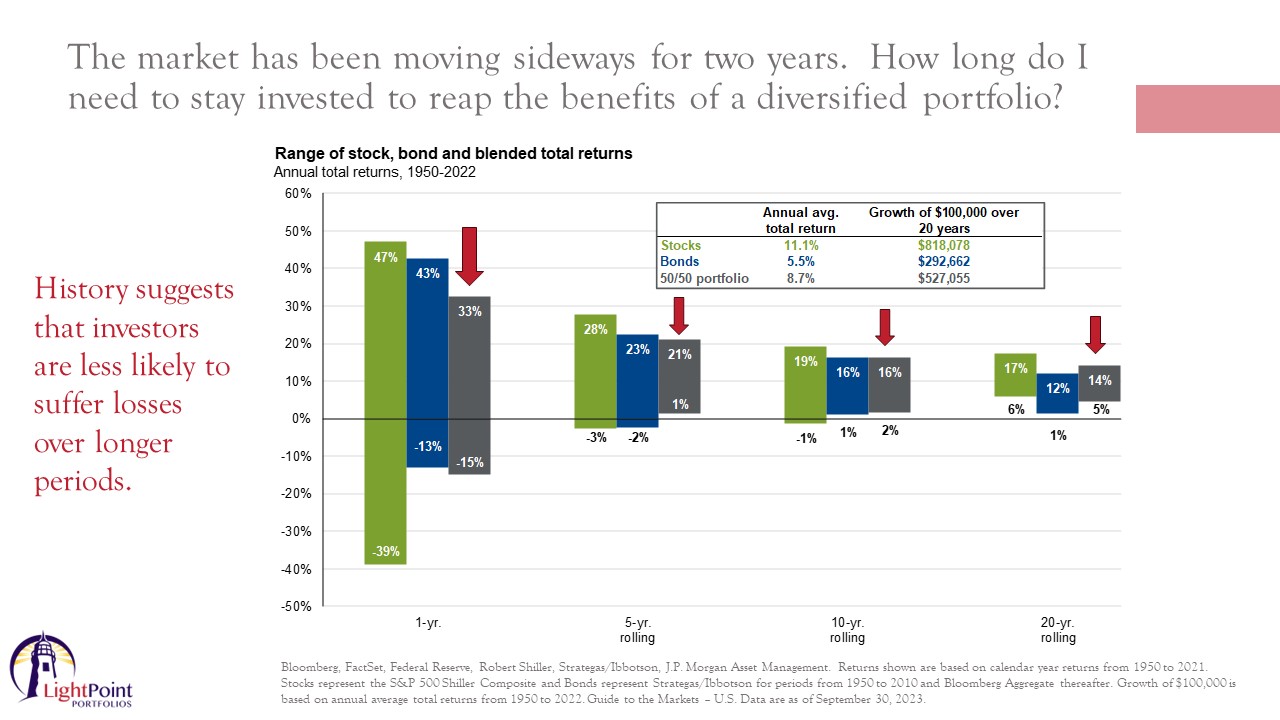

Okay, let’s move on to the next question. The market has been moving sideways for two years. How long do I need to stay invested to reap the benefits of a diversified portfolio?

Well, the value of maintaining a diversified portfolio is that good things come to those who wait, this chart illustrates that concept.

The green bars show the range of returns for a portfolio invested in stocks. The blue bars indicate an investment in bonds, and the gray bars show a blend of 50% stocks and 50% bonds.

So pretend that you are an investor with a portfolio 50% allocated to stocks and 50% allocated to bonds while one year returns have varied widely since 1950 – so a positive 33% to a negative 15% in any given year – that same blend has not suffered a negative return over any five year, 10 year, or 20 year rolling period over the past 70 years.

History suggests that the longer you stay invested, the less likely you are to suffer losses. So if you have been with us for only a few months or a year or even two years, that’s not enough time to reap the benefits of having a diversified portfolio.

And finally, probably the most commonly asked question I’ve received, what is your outlook for the rest of the year?

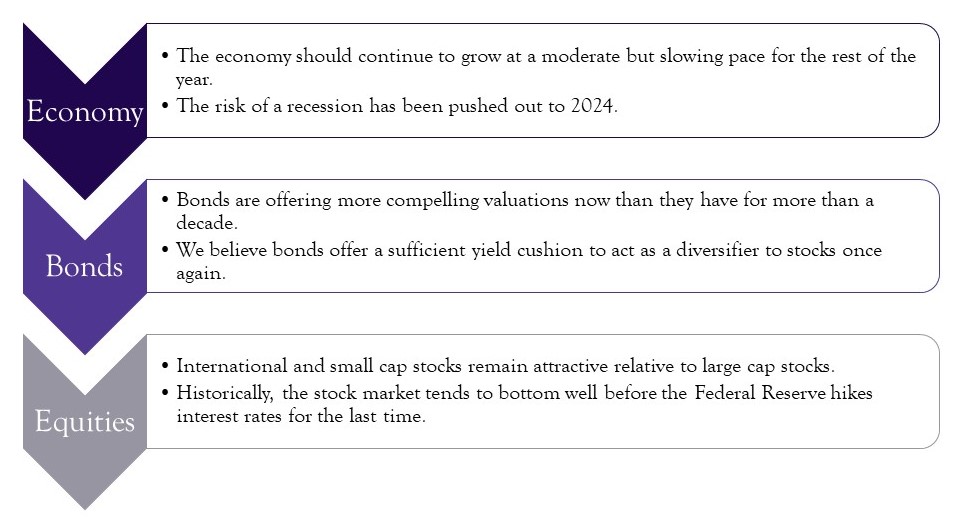

Well, in terms of the economy, economic growth has been impressive this year and the third quarter has been no exception. Business spending has held up better than expected despite tighter lending standards. Unemployment continues to hover around 50 year lows. The housing market appears to have stabilized but remains tight. Consumers have remained resilient, supported by a tight labor market and rising real wages, but they have been depleting their savings and taking on more debt to maintain their current lifestyles.

Higher energy prices as well as the resumption of student loan payments will put additional pressure on the average consumer heading into the end of the year. So while the labor market’s held up remarkably well, the strength of the consumer as well as the labor market is gradually easing. So overall, we do believe the economy should continue to grow at a moderate but slowing pace for the rest of this year.

Originally, we expected a recession to begin in 2023, but that has been pushed out to 2024.

What does that mean for the bond market and the stock market? Well, I’ve talked about the fixed income side extensively already, but just to summarize, we believe the Fed is near the end of its hiking cycle. The market has priced in one more rate hike in November, and a prospect of rates staying higher for longer than originally anticipated, which has caused that backup in returns as of late. If the economy avoids every recession, the Fed should be able to deliver mild interest rate cuts next year. However, if the economy enters a recession, maybe because the Federal Reserve is keeping interest rates too high for too long, they will be forced to cut interest rates rapidly in order to boost economic growth. So both outcomes should bode well for high quality fixed income investments.

Again, bonds are offering more compelling valuations now than they have for more than a decade, and we are planning to tiptoe into these areas over the next few months. Additionally, we believe that bonds offer a sufficient yield cushion to act as a diversifier to stocks, once again, should we get some exogenous shock that causes a large stock market selloff.

On the equity side, we haven’t been making significant shifts. While the markets have had solid gains in 2023, this rebound has not been evenly distributed, and it’s extremely important to note that more than 90% of the return of the S&P 500 index year to date has come from just seven stocks. While some stocks look expensive, there are plenty of stocks trading at attractive valuations relative to the broader index, which is when active management tends to shine. Valuations still look better compared to the end of 2021, and some asset classes look more attractive than others.

For example, international equities continue to trade at a historical discount to US stocks and small cap stocks are trading at a significant discount to large cap stocks. With inflation trending lower and the fed near the end of its tightening cycle, in our opinion, those are two key positives that we expect to provide support to equity prices. Historically, the stock market tends to bottom well before the Fed hikes interest rates for the last time. So we are cautiously optimistic heading into the last quarter of this year.

I hope this presentation was helpful for you. As always, thank you for your continued confidence and please reach out to us with any questions that you may have.

Do you know what business practices you are supporting through your current investments?

Want to learn more about how your faith can impact how you handle your finances?

Call us today! (540) 345-3891