How do investors’ thoughts and emotions affect stock and bond prices?

In our October 2022 market commentary, Beacon Wealth Consultants’ Chief Investment Officer Hillary Sunderland, CFA®, CKA® explains investor sentiment, answering:

- What is investor sentiment and why do we use it?

- What does investor sentiment look like in today’s market?

Thank you for your continued confidence and please reach out to us with any questions you may have.

Full transcript below.

Transcript

Hi, my name is Hillary Sunderland and I’m the Chief Investment Officer of Beacon Wealth Consultants and LightPoint Portfolios. This is your October 2022 update.

Well, once a quarter, I like to answer a question that we’ve received from one of our valued clients, and this month’s question really has to do with investor behavior and how you’re feeling about the market, whether you are optimistic or pessimistic, and how that can impact stock market trends. So the actual question is, you often talk about investor sentiment in your market commentaries, what is this and why do you use it?

Well, when I talk about investor sentiment, what I’m referring to is the attitude toward the market at a given time, investors can be overly optimistic, pessimistic, or somewhere in the middle, and we look for extreme readings in sentiment because those tend to be contrarian indicators in the market.

Remember that in a freely traded market, only those participants who actually buy or sell a security have an impact on its price, and the greater the volume of a participant’s trades, the more impact that market participant will have on its price.

So to illustrate this, I want you to think about the game of Monopoly. People who are statistics inclined know that the orange properties, New York Avenue, Tennessee Avenue, and St. James Place are some of the most important properties to own on the board because they are the most likely to be landed on by other players. So if you sit down and play a game of Monopoly with my family and these properties go up for auction, you would see that the price of these properties will be bid up. And Monopoly is an example of a freely traded market in action as more people are willing to buy a property, the price for the property increases. Well people do the same thing with stocks and bonds, but they do it on both the buy side and the sell side.

I’m a student of behavioral finance, and what behavioral finance studies show is that when it comes to investing, cognitive biases and behavioral biases influence people to do the wrong things at the wrong time. For example, people seem to be hardwired to exhibit what we call herd mentality, and that refers to investors’ tendency to follow and copy what others are doing, and people can become influenced by their instincts and their emotions rather than by rational analysis.

Let’s take a quick look at how people exhibit herding bias. Suppose you go to a fair and it’s full of food stands and you’re looking for a place to grab a slice of pizza. There are two food stands in front of you. Which one do you choose? The one that has a longer line and tables beside it that are full of people, or do you choose the food stand with a lot of open tables where you can walk right up to the counter?

Well, when asked, most people would choose the busy food stand over the relatively empty one because most people assume that the busier food stand must have better food. And that may or may not be true. Perhaps the busier food stand is just full because one very large family decided to eat there. But regardless, you are likely making your decision of where to eat based on the decision of others.

The key thing here is that we are hardwired to herd, and there’s a lot of evidence of herd mentality in financial markets. Investors will buy into areas of the market such as tech stocks during the dot-com bubble or cryptocurrencies in late 2020 or early 2021 because everyone else was buying into them and they had a fear of missing out. They are exhibiting overconfidence that the upward trend will continue and are trading on market noise and emotions. What behavioral finance shows is that the more extreme the optimism in financial markets, the lower the expected returns on average.

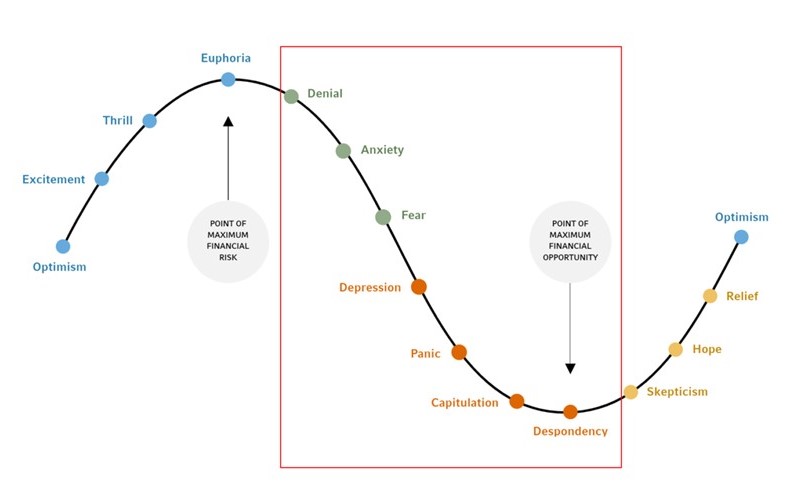

And the same thing happens on the sell side. Investors actually find it to be emotionally or psychologically painful to go against the crowd because it triggers the fear that if everyone else is selling and I don’t, and I’m hanging on, they might know something that I don’t and I might make the wrong decision if I go against the crowd. And this is what’s illustrated by this red box here and a bear market like we’re in now.

Investors first go through denial that the market is even selling off at all, and then they tend to have a bit of anxiety about it. That anxiety leads to fear where that herd mentality really starts to kick in. Fear leads to depression. Depression leads to panic. Panic leads to what we call capitulation, where the market is at the point where everyone is going to throw in the towel and sell regardless of the price they’ll receive.

Then goes ahead and does it, and that leads to despondency. The point at which investors have lost all hope that things are going to turn around, and this is what we call the point of extreme pessimism and the more extreme the pessimism to higher the expected returns on average as these extremes and pessimism tend to occur near market bottoms.

So to summarize, both extreme optimism and extreme pessimism lead to mispricing, which is eventually corrected by market fundamentals. And this is why we look at measures such as investor sentiment because it provides us with a good guide for when to consider rebalancing portfolios or when to make incremental shifts within the portfolios. And we can assess this measure of sentiment in a variety of ways. We can look at money going into or out of mutual funds, put call ratios, or the AAII sentiment surveys.

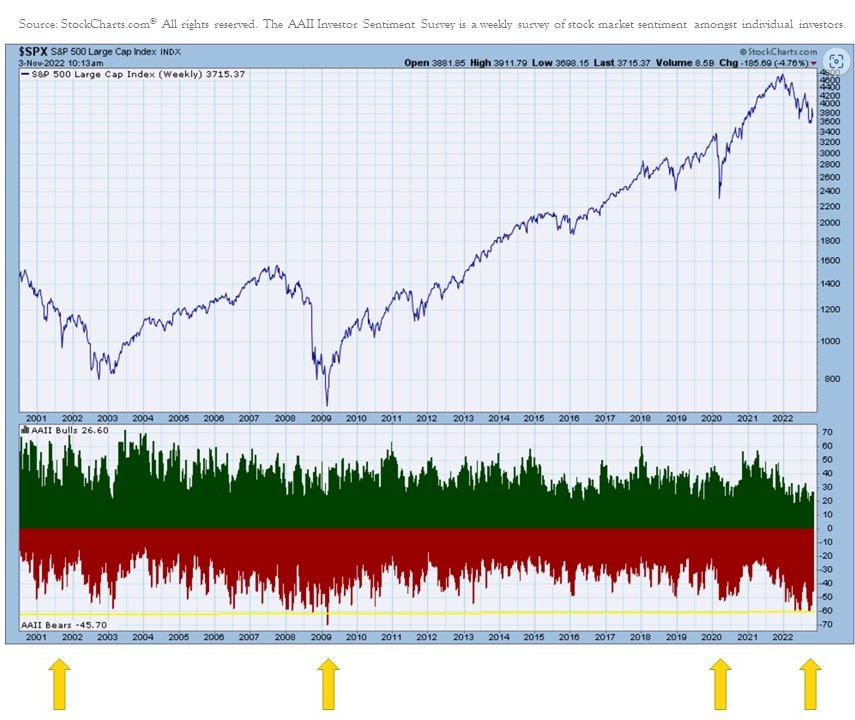

I’m not going to dive into all those on this video, but I just wanted to show you one of the more common ones to show you where we are currently. So portfolio managers often joke that stocks are the only thing in the world that can go on sale and nobody wants to buy them, and we certainly have a lot of stocks on sale right now.

Long-term measures of sentiment have continued to move downward throughout the year as shown by the red bars in the bottom of this chart. In mid-October, we hit levels where almost 60% of investors surveyed by this firm, this is the AAII investor sentiment survey. Almost 60% of investors had a bearish outlook on the markets, meaning they thought that the markets would be lower in the next six months than they were currently. It came off those levels a bit as the markets rallied in October, but in mid-October, that was a very poor outlook, and I wanted to put this in perspective for you.

We saw sentiment levels in mid-October that were worse than they were during the Covid 19 pandemic, which had a way more uncertain outcome than what is happening right now. The sentiment levels in mid-October were similar to the same levels experienced during the depths of the global financial crisis where the global banking system itself was in jeopardy and the sentiment levels were worse than they were after the September 11th attacks, which ushered in significant global uncertainty.

So hopefully this shows you that the fear in the markets right now is quite extreme and it illustrates that there is a lot of emotion going on, and this is the point at which people start thinking of a doomsday scenario for the markets as if it were the base case scenario. But when you step back from the emotions and take a look at the fundamentals, what we see right now is the S&P 500 operating earnings are flat when compared to last year, not down, but flat. Unemployment, still near historic lows. Consumers are in a good financial position relative to history and the doomsday scenario of a very bleak and prolonged recession, in our view is just not the most probable outcome.

Could it happen? Sure, anything could happen, but we manage to what is the most likely to occur, and we look across a range of possibilities. What we see right now is that in the United States, we are probably going to go into a recession, but it’s likely going to be a mild one. We do believe there will be a deeper recession in Europe, and we have repositioned portfolios accordingly for that.

Additionally, we think that some areas of the market have already priced in a recession, so areas such as small cap stocks and we overweight those areas. We also remain overweight alternative investments in most of our portfolios. Alternative investments can seek differentiated returns that have little to no correlation with stock and bond markets. And we are also overweight cash and are engaging and tax lost servicing as appropriate.

It’s important to keep in mind that historically both stocks and bonds have started to go up before the Federal Reserve is finished with raising interest rates. And additionally, the stock market usually bottoms before recession is even over. So we will continue to make adjustments to our portfolios as warranted by our outlook. We thank you for your continued confidence and please reach out to us with any questions you may have.

Would you like your investments to have a positive impact on the world? Give us a call!?

Do you know what Business Practices You Are Supporting through your Current Investments?

Or Contact Us to Schedule a Phone Call or Meeting.

Call us today! (540) 345-3891