In our latest interview, Chief Investment Officer Hillary Sunderland provides an insightful recap of the first half of 2024, highlighting the S&P 500’s impressive 15% rise driven by a select few stocks.

She also discusses the potential impact of AI, the economic outlook for the remainder of the year, and offers valuable advice on navigating market volatility during the upcoming election season. Tune in to get the full breakdown and analysis!

(Full transcript below)

Transcript

Cassie Laymon:

Hillary, can you even believe that it is the second half of the year already?

Hillary Sunderland:

No, it went by quickly. Cassie.

Cassie Laymon:

So we’re going to talk today a little bit about the markets, and let’s just start off by talking about what has happened in the first half of 2024. Can you give us the update?

Hillary Sunderland:

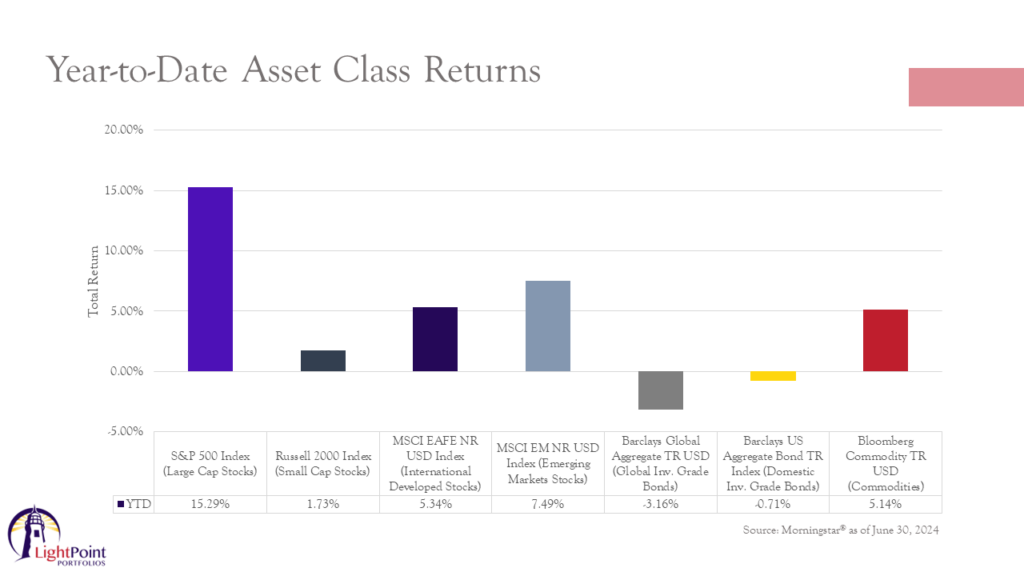

Sure. So equities maintained their upward trajectory and the S&P 500 notched multiple new all-time highs during the second quarter. For the first half of the year, the S&P 500 was up just over 15%. However, a significant portion of the gains came from just a few stocks in the index.

Domestic small cap stocks were up just under 2% as that higher for longer interest rate environment kept small cap stocks in a frustrating sideways trading range for about three years now. Abroad, both developed and emerging market stocks had returns in the mid single digits.

And then on the fixed income side of the equation, bonds staged a small rebound in the second quarter as inflationary pressures continued to come down, but there’s still slightly negative year to date, again, given that higher for longer interest rate environment. And then finally, to round out all the asset classes, commodities produced a mid single digit return in the first half. So overall, it was a decent first half for some areas of the market. It has been an environment though, where what you owned made a lot of difference because such a small percentage of the stocks in the index were responsible for a large portion of the gains year to date.

Cassie Laymon:

Okay. So when you say a number of these stocks, a small number of the stocks were responsible for the gains. Can you talk about that a little bit more? Tell us why is that and does it cause any kind of concerns for you in the future? Are you worried about that at all?

Hillary Sunderland:

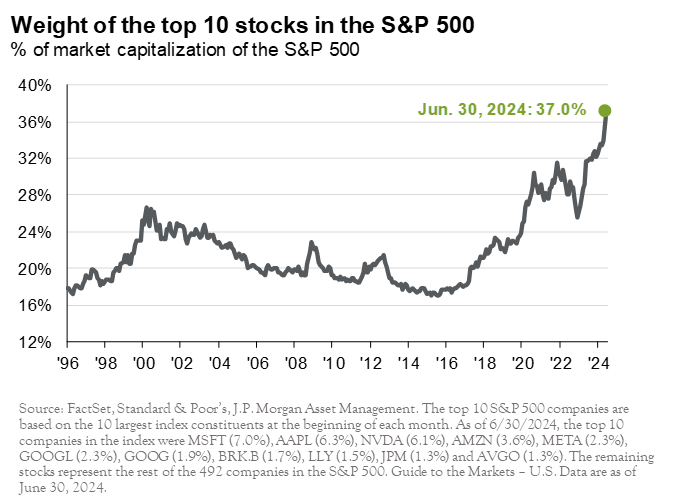

Yeah, it’s a good question, Cassie. So in a market capitalization weighted index like the S&P 500, what happens is that as the price of a stock increases in value, it increases that company’s weight in the index. And as a result, the companies that are performing the best get a larger and larger weight in the index, and therefore they have a bigger and bigger impact on their performance. So as of the end of the second quarter, the top 10 stocks in the S&P 500 comprise an astonishing 37% of the index. So to put that into perspective, if you were to invest $100 in the S&P 500 index today, about $37 of that is funneled to the stocks of just 10 companies, which is very high in comparison to history as you can see on this chart.

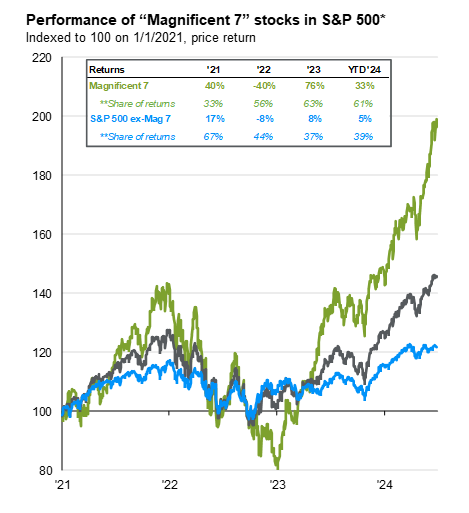

What’s happened over the last year or so is that there has been a lot of excitement concerning artificial intelligence. So AI has the potential to be applied broadly across businesses and increase productivity across a range of industries. And this excitement has led to a huge rally in just a few companies that are at the forefront of that growth. So companies like Nvidia, Microsoft, and Apple to name a few, these companies have been dubbed the Magnificent Seven. What you can see is the performance of this group of stocks, the Magnificent Seven, has just been massive over the last year, especially year to date. So the green line on the left hand side of this chart shows the performance of the Magnificent Seven, whereas the blue line shown here is the performance of the rest of the index. If you take out the effect of those seven stocks and you can see what a significant portion of the gains is coming just from those few names.

This has led some to question if this huge rally and just a few names is similar to the dot-com bubble, back in late 1999, early 2000. During the dot-com bubble, there was rampant speculation about internet companies and excitement around that, and that led to very large gains in stocks over a short period of time, and it ended badly for many investors.

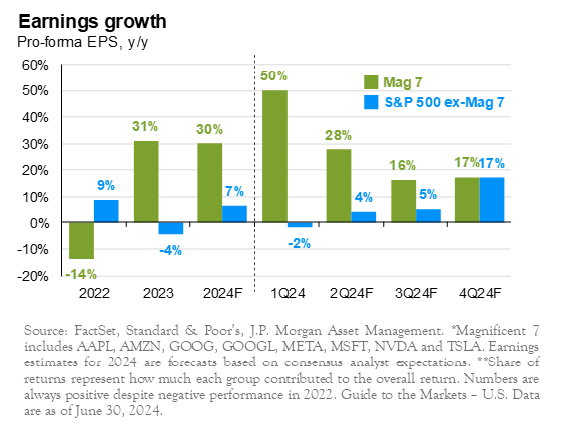

So I think in terms of thinking through this and is this an issue going forward, one of the things to look at here is whether or not the prices of these stocks have gotten ahead of themselves. And one way to look at that is to look at whether or not they’re trading based on expected future earnings.

The chart on the right here shows the earnings growth of the Magnificent Seven in comparison to the rest of the market.

And as you can see, the earnings growth has been quite robust for these companies in 2023 and is forecasted to continue for 2024. So in contrast to that internet bubble AI beneficiaries today are already very profitable companies that make their money by selling key infrastructure to businesses who are really looking to ramp up AI in their own businesses. So all that being said, we don’t expect just a few companies to continue to account for the majority of the gains going forward. If earnings forecasts are correct as 2024 progresses, earnings should broaden out across other sectors as seen by the blue bars here on this chart, and this should broaden out participation in the stock market as a whole.

Cassie Laymon:

That is so interesting, and I appreciate your insight about how this is really different from the dot-com bubble, those of us who lived through it, it’s really interesting to make that comparison. I appreciate that. Okay, so you’ve talked about where we’ve been so far this year. Tell us what is on your radar? What are you anticipating for the rest of 2024?

Hillary Sunderland:

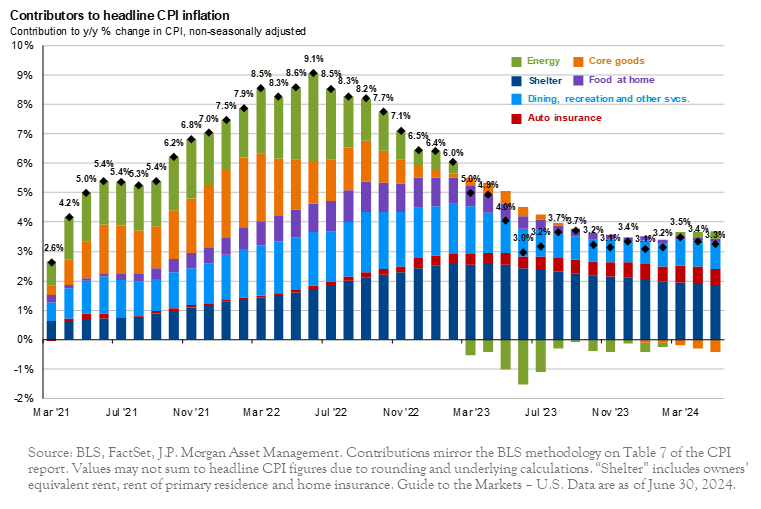

Sure. So in terms of the economy, we believe we’re on a path of sustained economic growth and stability. Inflationary pressures are starting to come down in key areas. Unlike what we saw throughout much of 2022 when inflationary pressures were broad based across the economy. The sticky inflation we’re now seeing is really based in just a few areas as shown on this chart, the shelter, insurance, and restaurant components of inflation.

But we believe that some of these pressures are likely to roll off over the next few months based on the data that’s coming in, and that’s going to give the Federal Reserve the room to reduce interest rates. Coming into the year, we expected that the Federal Reserve would reduce interest rates in the second half of this year. We are now there already, and that’s very much still on the table. We expect one, maybe two rate cuts before the end of 2024.

And that’s positive for a few different asset classes because bonds generally increase in price whenever interest rates fall. We’re constructed on bonds going forward, especially given current yields of upwards of 5% across most fixed income asset classes. And as interest rates come down, we do expect it to help other areas of the market as well, such as small cap stocks that I talked about earlier that have been stuck in the sideways trading range for three years. Once interest rates come down, that should really help that particular part of the stock market because those particular companies tend to be more pressured by higher interest rates. So interest rates coming down can be very constructive for many different areas of the market, and we’re continuing to look forward to that.

The other thing in the second half of this year, I’m sure that’s on your mind, is the election. Usually heading into election we see quite a bit of stock market volatility as there’s a lot of uncertainty surrounding what’s going to happen with the election, but I just want to caution investors to not let their politics influence their investing decisions. Ultimately, it’s policies, not politics that determines what happens in the markets and over long periods of time and through many, many cycles really doesn’t matter too much who wins the election, it’s more what policies go into place afterwards. And there are pros and cons to both sides, so stay tuned on that. I’m sure we’ll be giving an update on that as we get closer to November.

Cassie Laymon:

Very good. Yeah, I was going to say the next time we’re going to get together is in October to do the third quarter market commentary. We’ll be very closely election, so it’ll be interesting to hear what’s happened over the next couple of months and get your thoughts about that as we get closer. So thank you for your time. Thanks for bringing us up to date on your thoughts, and we’re looking forward to the next half of the year ahead.

Hillary Sunderland:

All right, thanks, Cassie.