Our first market commentary of 2025!

Hillary Sunderland and Cassie Laymon discuss the economic and market performance in 2024 and some thoughts on what’s ahead 2025.

Key points include:

- The US economy grew at a decent pace in 2024, with low inflation and a strong job market.

- The dominance of a handful of large tech companies (“the Magnificent 7”) has driven outsized market returns, but this trend may shift in 2025 if earnings growth slows for these companies and picks up for the rest of the market.

- The incoming administration’s proposed trade policies, such as higher tariffs, introduce significant uncertainty for 2025. Whether the proposed tariffs are actually implemented and, if so, their impact on inflation and the broader economy could be a major concern.

Watch the full video!

Full transcript below.

Transcript

Cassie Laymon:

Hillary, here we are in 2025. Happy New Year.

Hillary Sunderland:

Happy New Year to you, Cassie.

Cassie:

Well, I am really excited to hear your thoughts about what’s to come our expectations in 2025, but before we do that, I wondered if you could give us a little summary, a wrap up of 2024, what happened in the economy and the markets? Just give us a little summary of the year behind us.

Hillary:

Sure. Well, 2024 was an impressive year for both the economy and the financial markets. US economic growth continued at a decent pace. Inflation continued to drift lower except for it stalled a bit in the second half of the year, and the labor market remained strong with unemployment staying around 4%.

There were a lot of headlines and volatility throughout the year, as usual. We had some devastating hurricanes, a presidential, unlike any we’ve ever seen before, conflicts in the Middle East and the ending of negative interest rates in Japan also contributed quite a bit to volatility.

But overall, we had strong returns in the markets, as you can see from this chart, which shows the returns of major asset classes for the year ranked from the best performance to the worst performance with calendar year 2024.

On the far right, the clear winner again was US large cap stocks shown there in green with the S&P 500, returning 25% and building on a gain of over 26% in 2023, achieving two years in a row of returns greater than 20% is a rare feat.

It’s only happened four times since 1900. So it was quite the surprise that we had the runoff that we did in large cap stocks last year.

I do want to point out that the dominance of large cap stocks has been a bit of a headwind for our portfolios. Given our faith-based screening process, we tend to tilt away from that area of the market. But when we look at valuations across the globe, we believe that that dominance of just that particular asset class is likely to dissipate in years ahead.

Looking at some other areas of the market, small caps did well up a solid 11.5% further down the list. International developed markets in gray there lagged with only a 4.3% rise. It was hampered by currency weakness and concerns about tariffs following the presidential election.

And then finally bonds managed to eek out a small positive gain for the year. There was a lot of waffling concerning what the federal reserve’s going to do with interest rates in the year ahead, which caused quite a bit of volatility at the end of the year. We had a bit of a range bound market for that asset class in 2024.

Cassie:

Well, thank you. So I have a follow up question for you. You said that for two years that really large cap stocks have dominated returns. So why do you think that is and when do you expect that to change?

Hillary:

Sure, that’s a great question, Cassie. We’ve seen that continued dominance of just a few US tech companies in the market. Those tech companies are dubbed the Magnificent seven or the MAG 7, and a lot of it has to do with this artificial intelligence theme that has been playing out in the markets. I have a chart prepared to actually show this to you.

If you turn your attention to the left hand chart on this slide, you’ll see in green the returns of the Mag 7 and then the rest of the stocks that comprise a large cap segment of the market in blue. The performance of the index as a whole is in gray. There continues to be a huge gap in the performance of the Mag 7 companies versus the rest of the market. According to JP Morgan, they estimate that just seven companies contributed 55% of the performance in 2024.

So that’s down slightly from a 63% contribution in 2023. And the reason for this is the chart on the top right. When you invest in the stock market, you’re buying a future stream of earnings. In 2023, the Mag 7 companies grew earnings at 31% and in 2024, they grew earnings by 34%.

Meanwhile, earnings for the S&P 500 for the remaining stocks in the S&P 500 contracted by 4% in 2023, and it only grew by about 3% last year. So that’s a pretty large earnings gap. Now, why we think this dominance of just a few names will not last forever, is that in 2025 where that red arrow is pointing on this chart, earnings growth for the Mag 7 is expected to decelerate while the earnings other remaining stocks in the index are expected to accelerate.

And so that gap’s going to be closing over the years ahead and we believe that that will give us some much anticipated broadening out of returns and increase opportunities for active investors like ourselves. This is really an area where patients should pay off for investors, but it has been two years of solid returns for just one area of the market, which tends to be a little difficult for diversified portfolios.

Cassie:

Well, thank you for that clarification. And now of course, the thing we want to hear about is what is your outlook for 2025? We have a new administration coming in. They have this focus on tariffs and trade protectionism. What can we expect in the year ahead?

Hillary:

Yeah, great question, Cassie. So the incoming administration’s policy agenda is really looming large over the markets from a regulatory perspective. The incoming administration is committed to deregulation and tax cuts, both of which could boost profitability in certain sectors. And so you have certain sectors that are expected to do well depending on the regulatory agenda and other sectors that could suffer because of this.

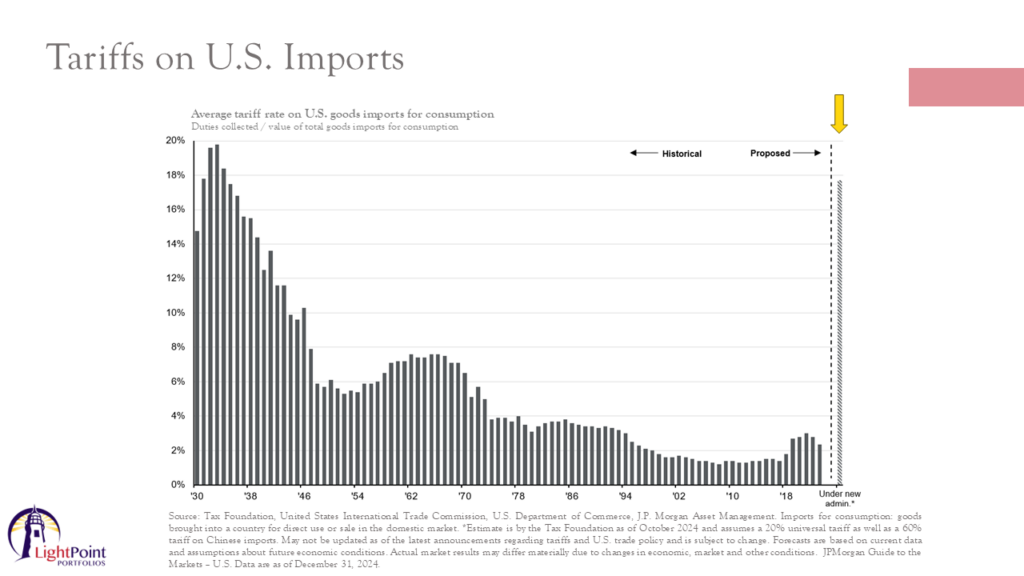

But I think the biggest unknown going into 2025 is really what’s going to happen around tariffs. Essential pillar of the Trump campaign has really been a renewed focus on tariffs and trade protectionism, which has introduced a significant amount of uncertainty, particularly for sectors relying on global supply chain. So I wanted to show you this chart.

This chart shows the average tariff rate on US goods import since the 1930s. And as you can see, the average tariff rate has steadily fallen over time.

But assuming that what has been proposed by President Trump is implemented, which is a 20% universal tariff and an additional tariff on Chinese imports of at least 60% calculations by the tax foundation, suggests that the average tariff rate on US imports could rise to 17.7% in 2025. So that’s up from just 2.4 in 2023.

Now, the tariffs are intended to be good. They’re intended to increase domestic production and generate additional tax revenue for the government. But if enacted as stated, that concern is really what will happen around inflation.

According to some estimates, enacting the tariffs as proposed could make inflation about 1.3 percentage points higher than it is today. So to translate that into dollars for the typical household in America, that’s roughly equivalent to an additional $1,200 per year for the average household, and that can be quite significant. And so it’s really that inflationary impact of tariffs that’s worrisome as well as we don’t know what the possible retaliation will be from trading partners, if that will reduce US exports and what that could effect that could have on the economy.

And so the outlook for the markets, I would say overall is cloudy at this point because we don’t know what will actually be implemented as is the case in politics. This could just be a proposed as a negotiation tool. They may not actually implement tariffs that are this high. We don’t know if the tariffs will be implemented permanently or if it will be just a shorter term negotiation tool. I think we are going to get clarity on this within just a few weeks. We’re only a few weeks away from inauguration day, and the impact of what actually gets enacted will be seen on the markets in short order.

And so we’re watching this closely and we’ll make changes to the portfolios as warranted, but really until we get some more clarity around what’s actually going to get through Congress, it’s a little murky at this point.

Although I will say that there are a lot of areas of the market where valuations to look good, there’s a lot of opportunity to pick up stocks that are trading at really good valuations, especially abroad. And so we’re looking into those areas to allocate assets toward in the new year.

Cassie:

Well, thank you for that overview, and it sounds like the next time we come together, we might have a little more clarity about what to expect in the year ahead. So thanks for taking the time to put that together for us.

Hillary:

Sure. Thanks, Cassie.

Call us today! (540) 345-3891

Do you know what business practices you are supporting through your current investments?

Want to learn more about how your faith can impact how you handle your finances?

Sign up for our newsletter!

Get news, market commentaries, videos, and faith-based investing articles from Beacon Wealth Consultants in your inbox.