Inflation, volatility, world events, Supreme Court decisions…2022 has been anything but boring so far. In our 2022 mid-year commentary, Beacon Wealth Consultants’ Chief Investment Officer Hillary Sunderland, CFA®, CKA® looks at where we are now and what we anticipate going forward this year. Hillary focuses on three questions:

- Does the economy look healthy going forward?

- Are stocks cheap or expensive?

- Are the market trends weak or strong?

We hope this update gives you hope and confidence to stay the course during these trying times. Thank you for your continued confidence.

Please reach out to us with any questions or worries that you may have, it is our pleasure to walk with you through times like these.

Full transcript below.

Transcript

Hi, my name is Hillary Sunderland and I’m the Chief Investment Officer at Beacon Wealth Consultants and LightPoint Portfolios and this is your 2022 midyear update.

Well coming into the year, we faced multiple shocks, including the impacts of China’s zero COVID-19 policy, the Russian invasion of Ukraine, continued supply chain issues, and inflationary pressures. And this has led to a very challenging and frustrating market environment for investors and asset managers alike.

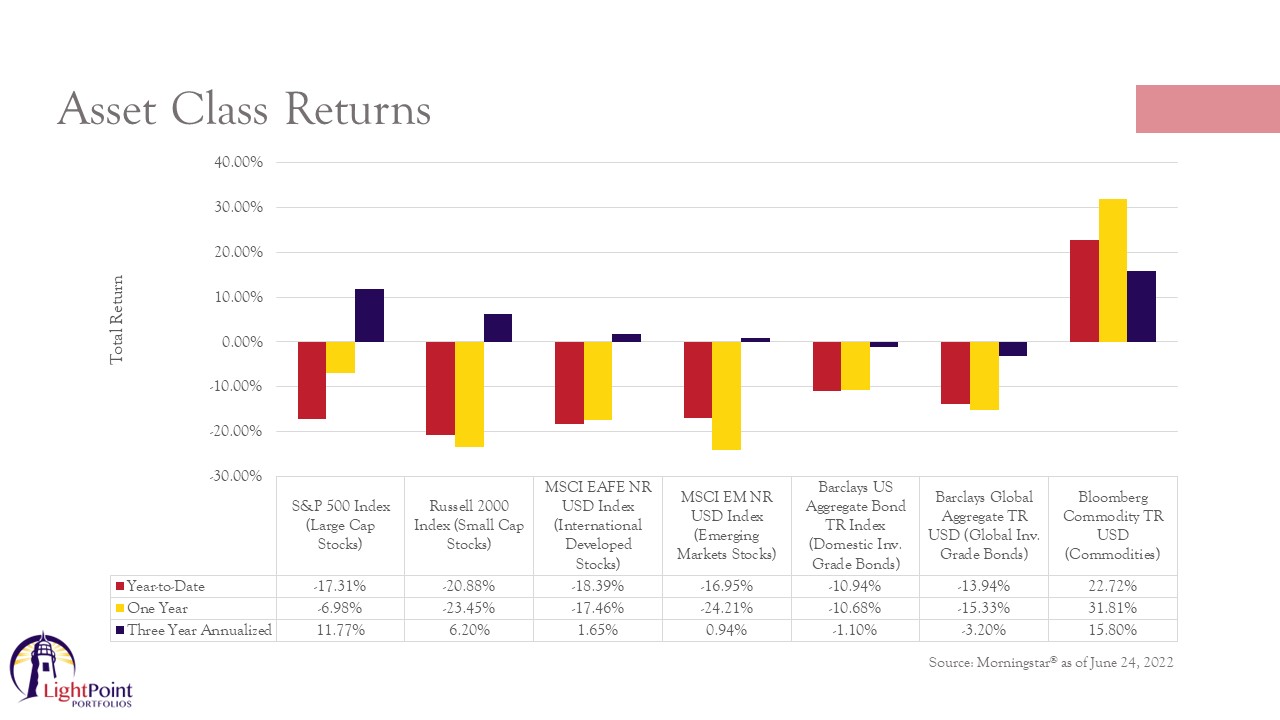

This chart shows the performance through June 24th, 2022. And as you can see from the red bars, which show the year-to-date returns, starting on the left domestic large cap stocks, small cap stocks, international developed stocks, emerging market stocks, domestic bonds, and global bonds have all suffered double digit declines. The only bright spot so far in 2022 has been commodities due to their inflation hedging capabilities.

Now, we did expect to see a correction sometime in the first half of this year, as one was long overdue, but it went a little deeper than we thought it would with the markets now dipping into bear market territory, which is defined as a drop of at least 20% from a recent high.

Now we are off those lows a bit, but unfortunately, it’s still been a very difficult investment environment overall. Unfortunately, many of those pressures — the supply chain issues, inflationary pressures and the Russia-Ukraine conflict — many of those pressures are still here. But one thing that’s important to note is that the decline we’ve had in the markets comes on the heels of a very robust market advance from the COVID-19 selloff lows. While most asset classes have losses on a trailing one-year basis as well, which is a yellow bar shown there, three-year analyzed returns, the blue bars, look much better with domestic stocks advancing 11.77% on an annualized basis. In five-year returns, which I didn’t show here because the chart got a bit too busy if I added yet another data point, but if you went out five years, the returns look even better.

So on a quarterly basis, what I’d like to do is share some market insights and our outlook with you. We believe that any investment strategy should start with a broad assessment of the economy and the markets, but as you can imagine, these can be complex topics. So I’d like to simplify our insights by answering three key questions for you.

- The first being, does the economy look healthy going forward?

- Second, are stocks cheap or expensive?

- And third, is the market trend weak or strong, meaning is the market likely to change direction soon?

Does the economy look healthy going forward?

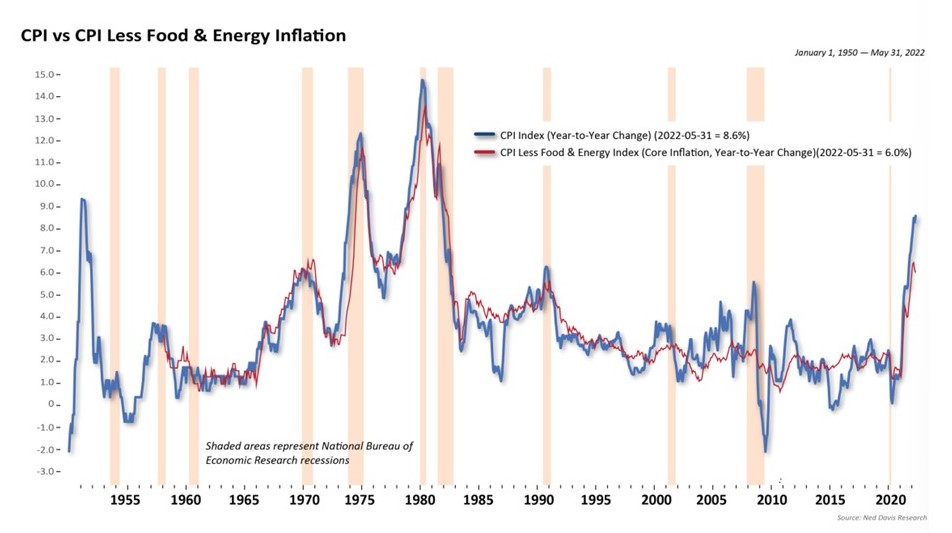

So let’s start with that first question here. Does the economy look healthy going forward? Well, the weight of the evidence is still supportive of economic expansion. Albeit one that is slowing because the Federal Reserve has had to raise interest rates to slow down inflationary pressures. Too much money chasing too few goods combined with supply chain distractions and a brutal Russian invasion of Ukraine has caused a nasty bout of inflation.

This chart here shows the CPI index as well as the CPI when you take out food and energy, which tend to be the more volatile components of inflation. In May, the CPI print was the highest in 40 years, which led the Federal Reserve to hike interest rates by 0.75%, just a few weeks ago.

Now, one thing to note in looking at inflation in the U.S. since the 1950s, as this chart shows, is that we’ve experienced four larger bouts of inflation, which you can see here by the bigger spikes, but note the symmetric nature here: once peak inflation was reached, it declined as fast as it rose. And I don’t think we’re going to have inflation that lasts for years on end. This is not the 1970s. The labor markets are structurally different, advances in technology can keep inflationary pressures down over the long term. And the Federal Reserve has indicated they will do what they need to do to bring inflation under control.

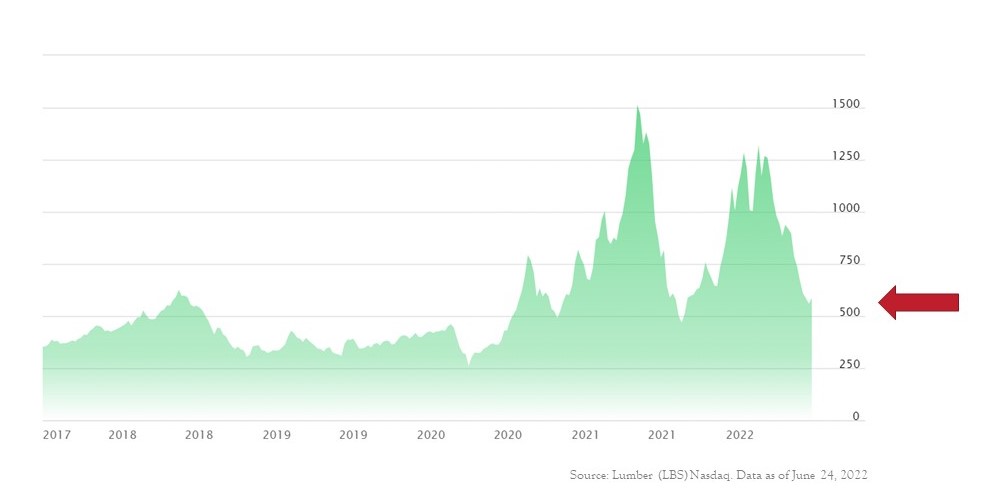

I do expect inflation to moderate in the second half of the year provided there’s no escalation in the Russia conflict. Other than food and energy costs, other commodity prices are easing. So just look at the price of lumber, which made a lot of headlines over the last two years because it really increased the prices of home building. The price of lumber is down over 50% year to date and it’s near levels from 2020.

Shipping costs and delay times have come down for goods at a time when consumers are demanding less goods and switching more of their spending to services. Home sales have been moderating as well.

So one of the questions to ask here is why would the prices of durable goods such as washers and dryers and refrigerators continue to rise if consumers are exhibiting less demand for those items, while inventories are starting to increase? They shouldn’t.

And additionally, we are seeing a cooling in the labor markets, including the wage gain. So combined, I do think that all these forces should help ease inflationary pressures in the second half of the year.

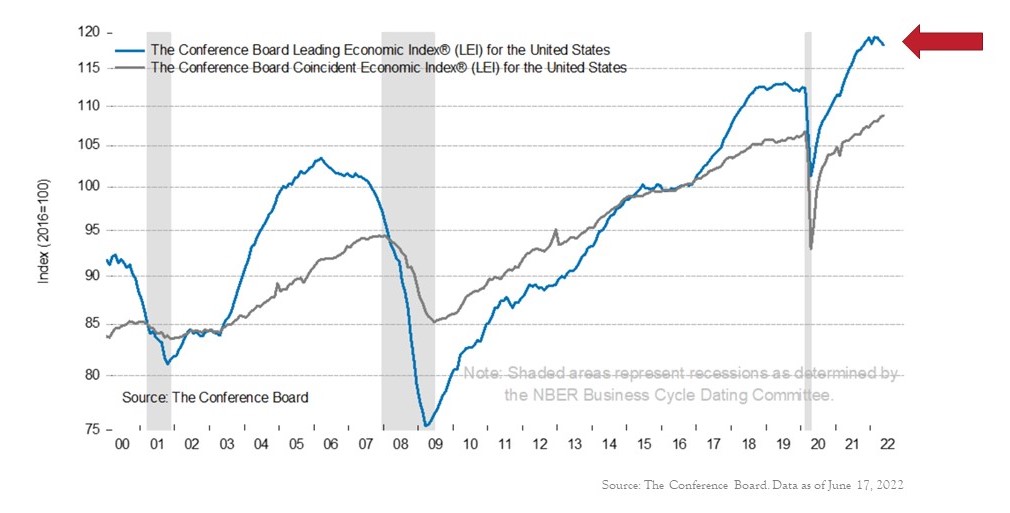

So looking now at the broader economy, this is the Conference Board’s Leading Economic Indicator (LEI) index or LEI. Zone in on the blue line here.

Typically it turns down and trends down for some time prior to a recession beginning, which is indicated by the gray shaded areas. Currently, the LEI paints a picture of slower, but continued economic growth. The LEI hit an all-time high in March and slowed slightly in both April and May suggesting that weaker economic activity is likely over the near term. However, this does not mean that we expect the economy to collapse.

There’s still plenty of pent-up demand for travel, leisure, and entertainment after the pandemic. Now, if you watch the news each day, you might be of the belief that we are already in a recession. In fact, a survey came out just a week or two ago, that found that 56% of the people surveyed thought that we were already in a recession. And that was just an amazing statistic to me because we have 3.6% unemployment. There are currently twice as many job openings in the United States as the number of people who are unemployed. So during a recession, what do you typically see? In a recession you typically see “going out of business” sales signs. All we see right now are “help wanted” signs.

A recession occurs when there’s not enough demand, inflation occurs when there’s too much demand. So, which is it, which narrative are we following here? While the odds of recession have certainly increased over the last few weeks, I don’t think we’re there quite yet. To me, this seems like more of a growth scare, similar to what we had back in 2011.

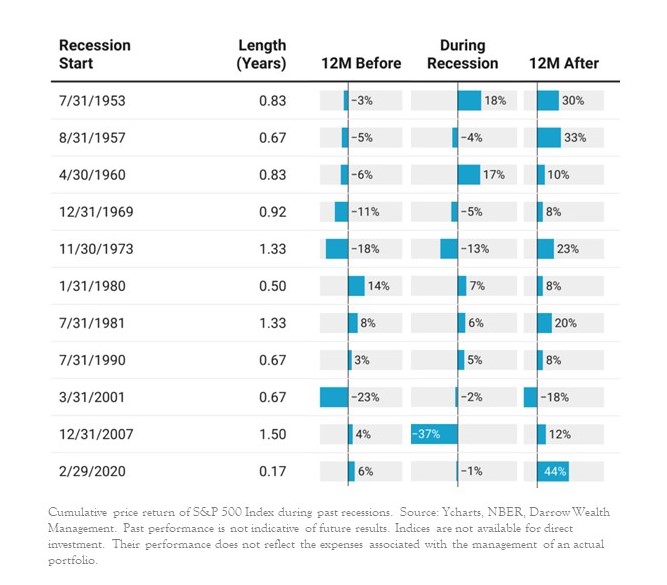

So you may be sitting here saying “Hillary, I don’t believe you. I think we’re in a recession already. And I’m worried about the stock market.” Well, interestingly, if you are worried about this, if history is any guide, by the time a recession is called, the market is already close to its bottom. This chart shows recessionary period since the 1980s, two thirds of the time, historically that we’ve had a recession by the time the recession was called, the stock market had already bottomed.

So for example, in the 1980s, recession was announced in June, but the stock market had already bottomed three months prior to that in March. During what’s known as the Great Recession of 2008, the market bottomed just two months after the recession was declared. Remember that the stock market leads the economy. It doesn’t always, it doesn’t follow the economy. It leads it. And so most time it’s ahead of what the economy is going to do.

How much does the stock market decline during a recession?

So, you know, all that being said, there’s no reason to think that if we do get a recession, that it would be as severe as 2008, which I think is anchored in most investors’ minds during that recession. So you can see here, the second line from the bottom, the stock market lost 37% during the recession. However, that was a global financial crisis whereby the global banking system was on the brink of collapse. And that’s not what we have right now, as you can see from this chart of the last 11 recessions. So going back to 1953, 45% of the time, the stock market actually has a positive return during a recession and 36% of the time the stock market had a loss of 5% or less.

Okay. So, you may be anchored in your mind that another 2007 scenario is likely to occur, but if you go back to the 1950s, typically you don’t get huge drawdowns during a recession, more likely your drawdowns in the market come before that as shown and in the 12 months before a column there, okay.

Now, if you hold on 12 months after recession, the market has positive returns 91% of the time. The lone exception here being calendar year being 2001 and that was largely due to the September 11th terror attacks. So if, and when a recession is finally declared, the most sensible approach is to not be scared of the “R word”, but to be disciplined and to ride it out.

I like the words of Dolly Parton in here. She wasn’t talking about a recession, but I think it’s appropriate. She said “the way I see it, if you want the rainbow, you got to put up with the rain.” And I think that’s a good indication here of what successful investors need to do. Investing success is achieved through time in the market, not by timing the market.

Are stocks cheap or expensive?

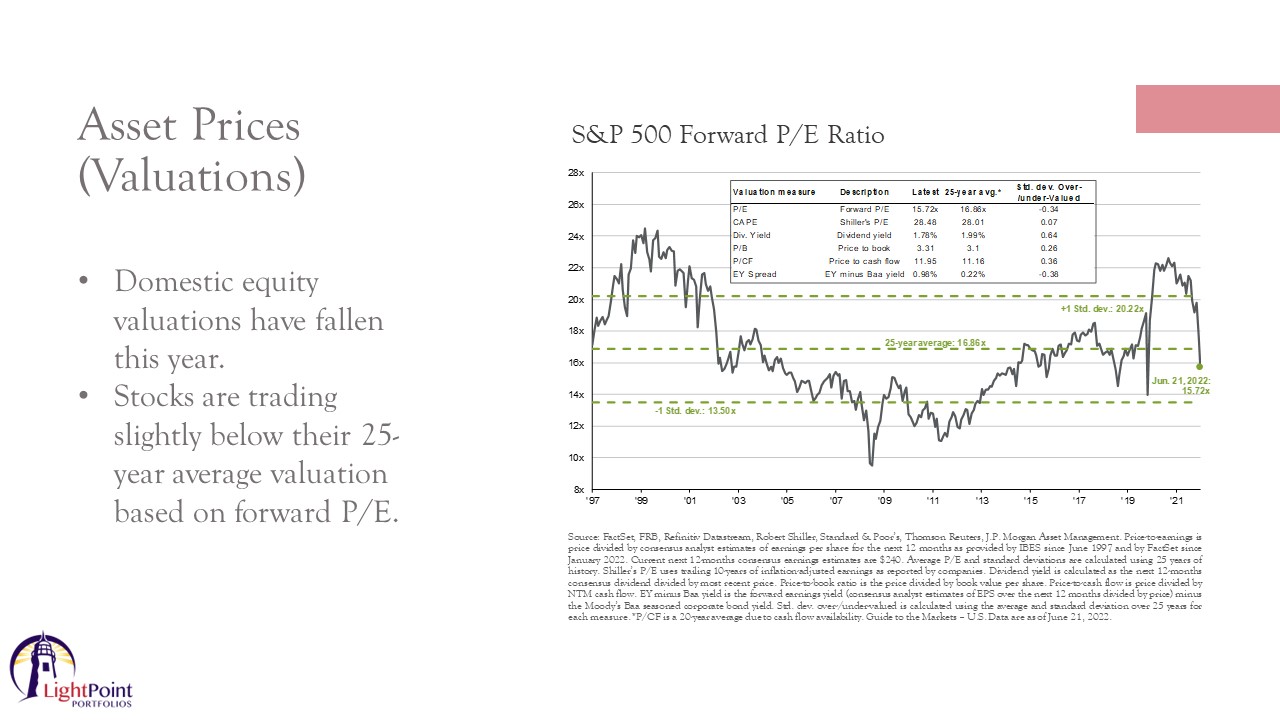

All right. So moving on to the next question, are stocks cheap or expensive? U.S. equity valuations, which is shown here, shows the S&P 500 forward price to earnings ratio historically. If it’s below its average valuation, that means it’s priced a little bit lower relative to its history in terms of how much you have to pay for a future stream of earnings whenever you’re investing in the stock market. So we’ve had a pretty large decline in valuations as shown on this chart.

Looking forward, rising interest rates, combined with a slowing economy, not necessarily a recession, but if we believe the economy is at least likely to slow, which I’m in that camp, it’s going to be difficult to justify an increase in valuations going forward.

Managers are going to need to be very selective in their approach to what types of stocks they are buying, because you’re going to want to buy stocks that can really defend margins in a continued inflationary environment, as well as be able to withstand any slowing growth in the economy.

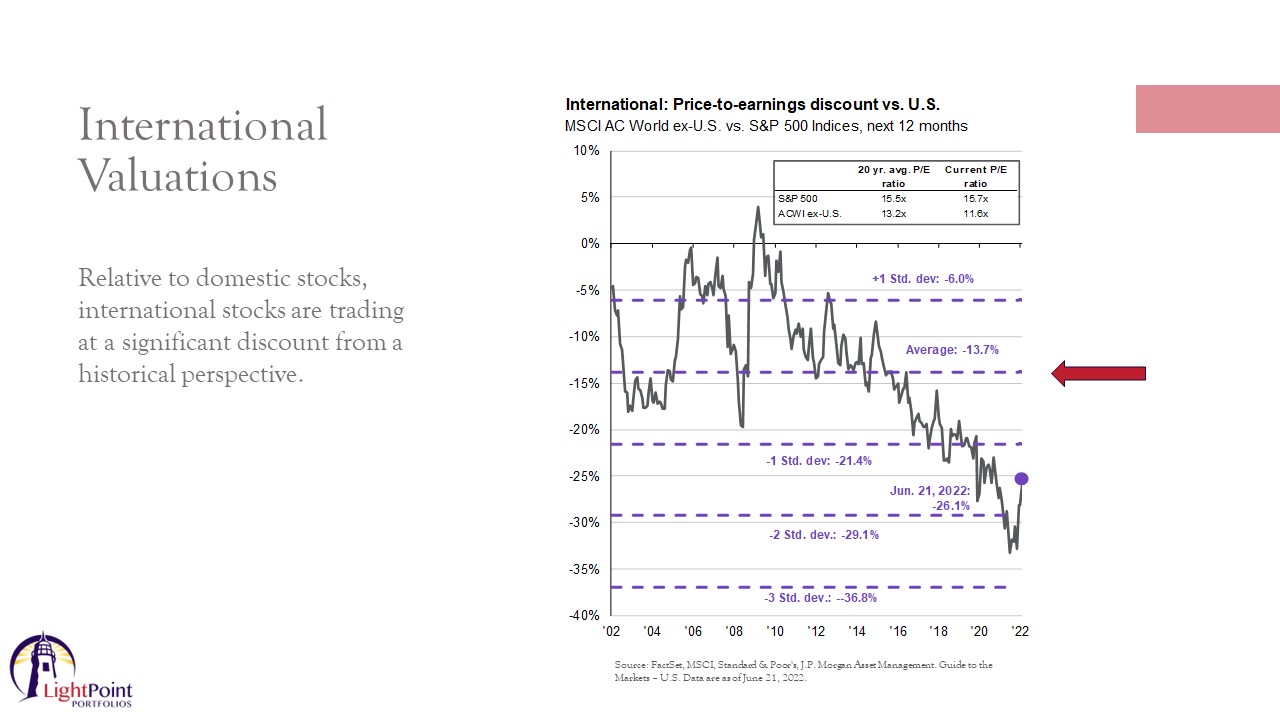

And so selection’s going to be key. Fortunately, we’re active managers. So we are already doing that for you on your behalf. Remember too, that we also invest globally for our clients. Valuations remain attractive with both emerging market and developed market stocks as some of their cheapest levels relative to the United States in the last 20 years as shown on this chart on the right. So this along with lower trade tensions and the prospect of a lower dollar over the long term argues for a greater allocation to international stocks and perhaps a return of international stocks outpacing domestic stocks.

How strong is the market trend?

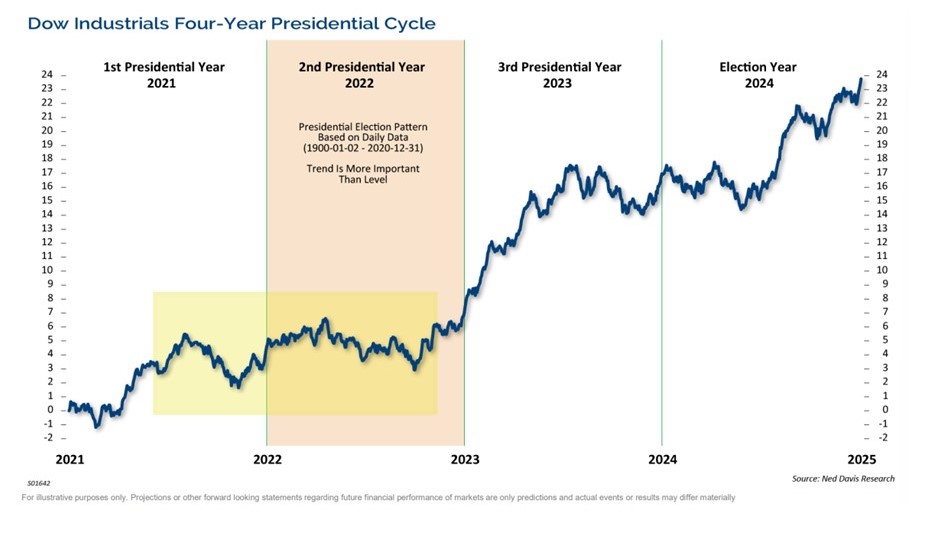

Final question, how strong is the trend? Meaning: are stocks likely to continue trading sideways or down? Well, currently the market trend is not good. We’ve been hitting a series of lower highs and lower lows. But it’s also important to remember that we are currently in the second year of Biden’s term, which is a midterm election year.

The midterm election year tends to be the worst year of the term for the stock market and mediocre at best. This chart shows the historical trend of the markets based on presidential election cycles, going back to the early 1900s, and then it’s overlaid by where we currently are within that cycle. The horizontal shaded zone shows that the market usually trades in a sideways trend leading up to the midterm elections.

Historically on average, since 1938, the market has endured a 20.98% correction into the midterm election year lows, which is right about where we were a week and a half ago. With the rebound rally, following those lows to the high of the next year, averaging 46.49%. So if you believe that we are in a period of slowing, but not contracting economic growth, that inflationary pressures are likely rolling over throughout the rest of the year, and that the market is likely to follow the usual path in a midterm election year, this is supportive up of a second half recovery. Once the markets establish a firm bottom. Now, obviously this is always barring an unforeseen economic shock.

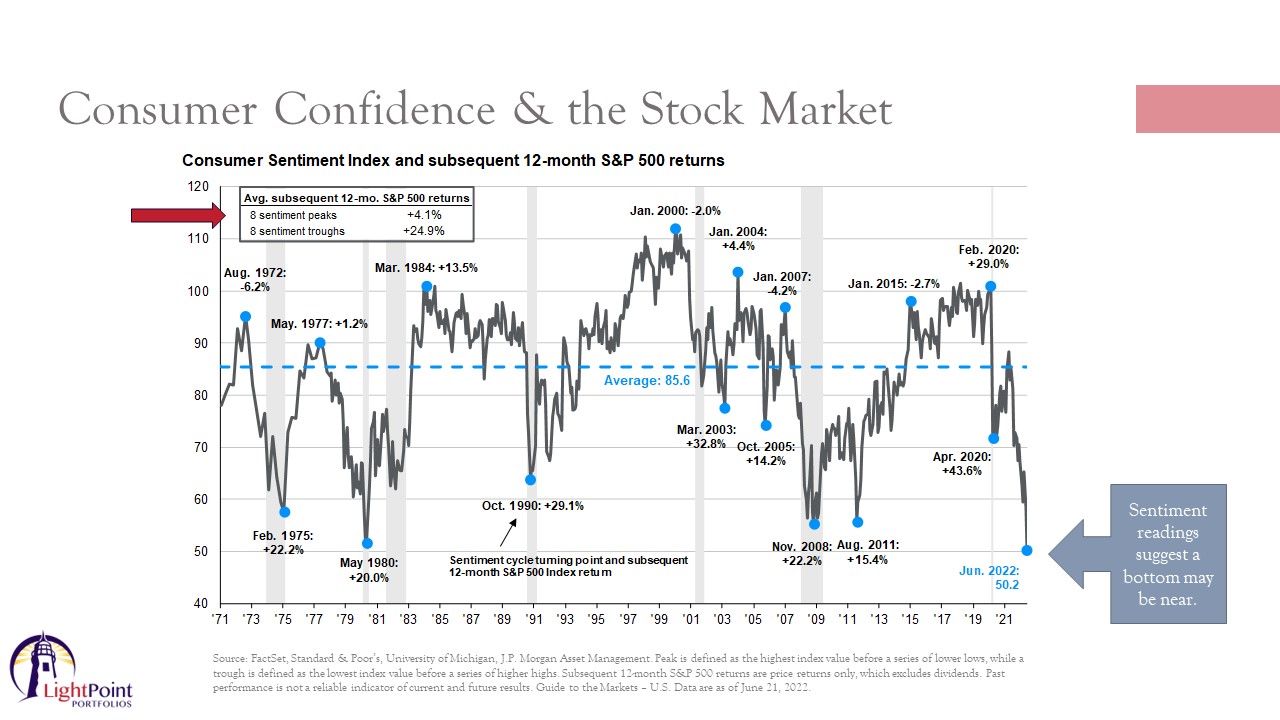

Consumer Confidence & the Stock Market

Okay. One more thing I wanted to touch on here is sentiment. When investors feel gloomy and worried about the outlook, their natural tendency is to sell risk assets in general and stocks in particular. However, history suggests that trying to time markets in this way is a mistake. Extremes in investor sentiment are contrarian in nature.

So when people are the most pessimistic that typically points to rebounds. This slide shows the University of Michigan Consumer Sentiment Index stretching back over the last 50 years. And there’s eight distinct peaks and troughs that are shown here and in the box in the upper left-hand corner there, where that arrow is pointing, we show how much the S&P 500 went up or down in the 12 months following the peaks or troughs.

So on average, when consumers are very confident and if you’re buying at a confidence peak, the return over the next 12 months averaged 4.1%. Okay. Now on the flip side, during the eight sentiment troughs, the average subsequent 12 month return of the S&P 500 was 24.9%. Now this is not to argue that U.S. stocks will return almost 25% over the rest of the year, many other factors will determine that outcome.

However, it does suggest that when planning for 2022 and beyond you really should spend your time focusing on your financial plan instead of how you feel about the economy. Because typically when investors let their emotions get the best of them, history shows they’re usually making changes in their portfolios at the wrong time.

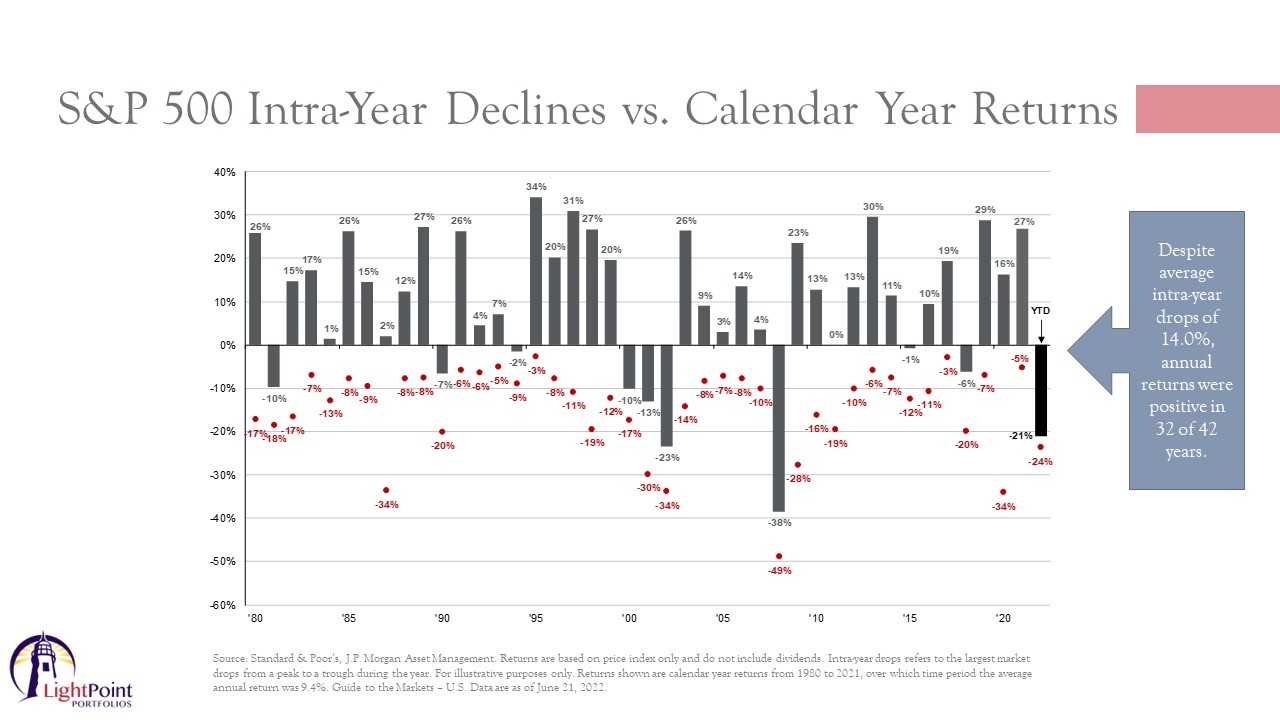

Overall investing is a bumpy ride, and it’s a normal part of investing. I’m going to end with this chart.

Since 1980, the red dots there show the intra-year decline of the S&P 500 within a calendar year. And the gray bar shows the return for the S&P 500 as of the end of that calendar year. Okay. So as you can see here, a draw down in the markets happens often, and some of them are very steep, but despite average intra-year drops of 14%, annual returns are still positive in 32 of 42 years. So 76% of the time, you still have a positive return by year end. So we thank you for your continued confidence and please reach out to us with any questions that you may have.

Do you have questions or concerns about the markets? Give us a call! We are here to help you understand and make decisions that protect and support your goals. It is our privilege to walk alongside you through times of uncertainty.

Contact Us to Schedule a Phone Call or Meeting.

Call us today! (540) 345-3891